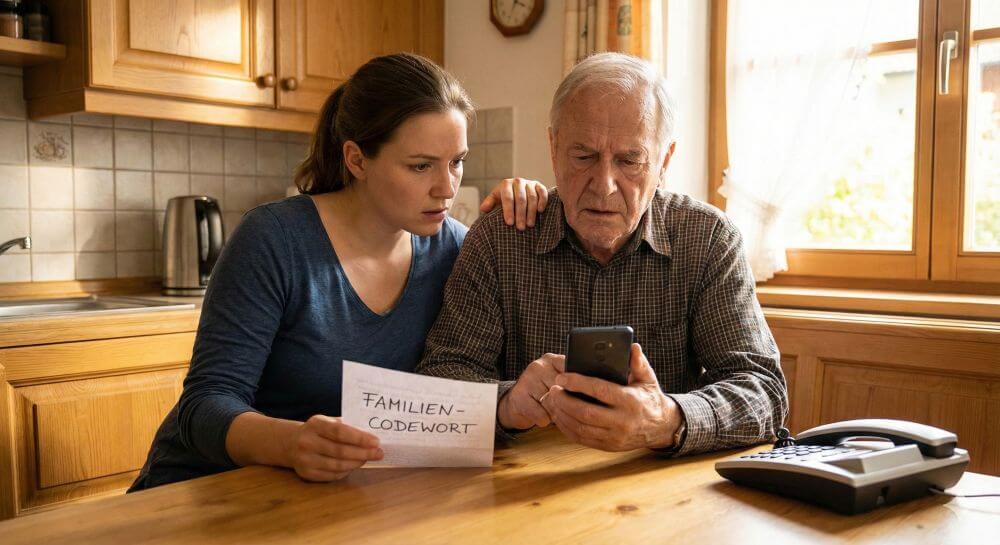

Abolition of Maestro cards – what does that mean

In the constantly changing world of Cashless payments is facing a significant change: the end of Maestro cards from July 1, 2023. In this article we will go into the differences between EC, Giro and Maestro and shed light on the effects of this change. We discuss what this change means for your future transactions, both domestic and international, and the options available to you in the post-Maestro era.

Abolition of Maestro cards – what does that mean

In the constantly changing world of Cashless payments is facing a significant change: the end of Maestro cards from July 1, 2023. In this article we will go into the differences between EC, Giro and Maestro and shed light on the effects of this change. We discuss what this change means for your future transactions, both domestic and international, and the options available to you in the post-Maestro era.

Do you know the difference: EC, Giro and Maestro?

Do you know the difference: EC, Giro and Maestro?

The original EC card has not existed since 2007. The name originally stood for “Eurocheque-Card” (until 2002), with which bank customers could withdraw money throughout Europe. In 2002, the abbreviation EC was adapted by the German banking industry to symbolize “Electronic Cash”. Although no changes were noticeable in Germany when shopping or withdrawing money, a popular function of the old EC card has been replaced by the new German Electronic Cash: the ability to withdraw money abroad, for example on vacation in Italy.

International systems such as Mastercard’s “Maestro” system replaced Europe-wide solutions to enable cashless payments worldwide. Many German bank cards were also provided with the red and blue “Maestro” logo. And despite this system change in the background, the bank customer often did not notice any change.

The official renaming of the EC card to “Girocard” in 2007 did not catch on everywhere in everyday language. According to the Bundesbank, the Girocard is the second most common form of payment in Germany after cash.

The original EC card has not existed since 2007. The name originally stood for “Eurocheque-Card” (until 2002), with which bank customers could withdraw money throughout Europe. In 2002, the abbreviation EC was adapted by the German banking industry to symbolize “Electronic Cash”. Although no changes were noticeable in Germany when shopping or withdrawing money, a popular function of the old EC card has been replaced by the new German Electronic Cash: the ability to withdraw money abroad, for example on vacation in Italy.

International systems such as Mastercard’s “Maestro” system replaced Europe-wide solutions to enable cashless payments worldwide. Many German bank cards were also provided with the red and blue “Maestro” logo. And despite this system change in the background, the bank customer often did not notice any change.

The official renaming of the EC card to “Girocard” in 2007 did not catch on everywhere in everyday language. According to the Bundesbank, the Girocard is the second most common form of payment in Germany after cash.

Why there will be no more Maestro cards

Why there will be no more Maestro cards

Mastercard, the company behind the Maestro system, has decided to phase out Maestro from July 1st. The US payment service provider wants to standardize its international business. In addition, the function is not sufficiently suitable for online trading and is therefore outdated, according to the company.

However, the consumer advice center suspects that Mastercard wants to achieve a larger share of online retail sales with this step. When paying with a Mastercard card, there are fees for the company.

Alternatives to Maestro for cashless payments abroad

Girocards without a Maestro function can be used only in Germany. Banks are now turning to other systems to facilitate payments abroad. Some have already made the switch. “Your bank must tell you when you can no longer use your Maestro card“, according to the consumer advice centre.

- V-Pay instead of Maestro: V-Pay, a product of the US company Visa, offers a similar function to Maestro. According to the consumer center, however, V-Pay is mainly aimed at the European market, while Maestro could be used worldwide. Therefore, Maestro was used more often as V-Pay. Some banks have already switched to V-Pay. Visa has previously stated that V-Pay will continue to be available.

- Two cards in one: With co-badging (payment instrument to which -usually one payment card- more than one payment brand is assigned), banks can use a debit card from Mastercard or Integrate Visa on their customers’ Girocards. In contrast to credit cards, debit card transactions are debited directly from the associated bank account. Girocards are therefore national debit cards, while Mastercard and Visa debit cards can be used worldwide.

- Abolition of the Girocard: According to the consumer advice center, some banks could abolish the Girocard entirely and only use the international debit card from Mastercard or Visa. In theory, these could also be used in retail, but so far not all stores have accepted these cards, the consumer advice center warns. “Merchants could also face higher costs as there are fees to the card company.” These fees are higher than with Girocards and could result in higher prices.

As is already the case with some accounts, banks could introduce a two-card system – with a Girocard for domestic payments and a debit or Credit card for use abroad.

Tip: Also read our Article about the digital euro

Mastercard, the company behind the Maestro system, has decided to phase out Maestro from July 1st. The US payment service provider wants to standardize its international business. In addition, the function is not sufficiently suitable for online trading and is therefore outdated, according to the company.

However, the consumer advice center suspects that Mastercard wants to achieve a larger share of online retail sales with this step. When paying with a Mastercard card, there are fees for the company.

Alternatives to Maestro for cashless payments abroad

Girocards without a Maestro function can be used only in Germany. Banks are now turning to other systems to facilitate payments abroad. Some have already made the switch. “Your bank must tell you when you can no longer use your Maestro card“, according to the consumer advice centre.

- V-Pay instead of Maestro: V-Pay, a product of the US company Visa, offers a similar function to Maestro. According to the consumer center, however, V-Pay is mainly aimed at the European market, while Maestro could be used worldwide. Therefore, Maestro was used more often as V-Pay. Some banks have already switched to V-Pay. Visa has previously stated that V-Pay will continue to be available.

- Two cards in one: With co-badging (payment instrument to which -usually one payment card- more than one payment brand is assigned), banks can use a debit card from Mastercard or Integrate Visa on their customers’ Girocards. In contrast to credit cards, debit card transactions are debited directly from the associated bank account. Girocards are therefore national debit cards, while Mastercard and Visa debit cards can be used worldwide.

- Abolition of the Girocard: According to the consumer advice center, some banks could abolish the Girocard entirely and only use the international debit card from Mastercard or Visa. In theory, these could also be used in retail, but so far not all stores have accepted these cards, the consumer advice center warns. “Merchants could also face higher costs as there are fees to the card company.” These fees are higher than with Girocards and could result in higher prices.

As is already the case with some accounts, banks could introduce a two-card system – with a Girocard for domestic payments and a debit or Credit card for use abroad.

Tip: Also read our Article about the digital euro

Beliebte Beiträge:

That’s why a VPN is worthwhile for everyone

Cyber attacks on the Internet are on the rise, and freedom on the Internet is at risk. A VPN can provide a remedy.

Cloud Working – what is behind digital collaboration?

The Internet is constantly evolving and has a massive impact on the world of work. In order for employers and employees to remain competitive in the long term, they must adapt to changing circumstances and use new technologies for themselves.

How does Conditional Formatting work in Excel

Many times, you have certainly wished that certain contents of your Excel spreadsheet be highlighted a little bit more, so that they catch your eye at a glance.

Create dependent dropdown menus in Excel

In Excel, it may make sense to create a drop-down list that is based on a data source and also adapts dynamically instead of creating a very long list in rows or columns.

Is the purchase of Office 2019 worth it?

We clarify the new features of Office 2019, and if and for whom it is worth buying.

Offers 2024: Word & Excel Templates

Beliebte Beiträge:

That’s why a VPN is worthwhile for everyone

Cyber attacks on the Internet are on the rise, and freedom on the Internet is at risk. A VPN can provide a remedy.

Cloud Working – what is behind digital collaboration?

The Internet is constantly evolving and has a massive impact on the world of work. In order for employers and employees to remain competitive in the long term, they must adapt to changing circumstances and use new technologies for themselves.

How does Conditional Formatting work in Excel

Many times, you have certainly wished that certain contents of your Excel spreadsheet be highlighted a little bit more, so that they catch your eye at a glance.

Create dependent dropdown menus in Excel

In Excel, it may make sense to create a drop-down list that is based on a data source and also adapts dynamically instead of creating a very long list in rows or columns.

Is the purchase of Office 2019 worth it?

We clarify the new features of Office 2019, and if and for whom it is worth buying.

Offers 2024: Word & Excel Templates